Parents and Tax Returns: What Should You Review?

summary

You just hit ‘Submit’ on your tax return… but you have no idea whether you did it correctly or left money on the table. Taxes were a breeze before you had kids. You had very few tax documents to gather, and answering the required questions from your tax software took half the time.

Now? You’re gathering documents or information for daycare costs, tracking contributions you made to 529 college savings plans, or navigating the Child Tax Credit for each child in your family. There’s so much more required from you, but not enough time without feeling stressed. Being a parent myself, I’ve been there!

As a tax professional, I’ve helped parents in their 30s and 40s prepare and file their returns. I’ve also reviewed hundreds of tax returns from parents, and nearly every one had at least one costly mistake. So, in today’s blog, I’d like to share the 5 parts of your tax return that you should certainly double-check before submitting.

your dependents: don’t forget your kids!

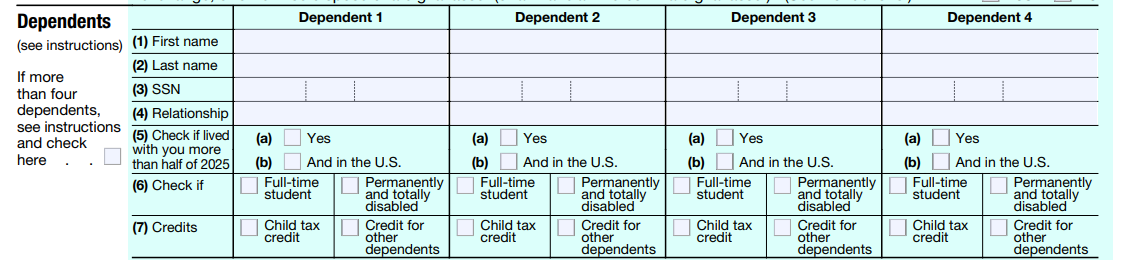

The dependents section of your tax return is located halfway down the first page of Form 1040.

Dependent Information on Your Tax Return

What Should I Review?

As straightforward as it sounds, you really want to double-check for the proper spelling and Social Security number of each dependent. I once reviewed a client's data in which she entered the same SSN for both of her children, so it does happen!

After you review the name and SSN, I recommend reviewing each dependent’s eligibility as either a qualifying child or a qualifying relative. A dependent is either classified as a qualifying child or a qualifying relative, each carrying a different set of “eligibility tests”. Your tax software likely asked you a series of questions about the potential dependent to determine whether they meet the requirements to be claimed as a dependent. Review these answers!

Why is it Important to Review Your Dependents?

Avoiding unnecessary delays or amending your return is the first reason as to why it’s worth your time reviewing the dependents section of your tax return.

In addition, dependents help you claim certain tax breaks, so failing to claim an individual may lead you to pay more in taxes than you otherwise should pay.

your deductions

Deductions are essentially “subtractions” from your income, meaning you do not pay tax on those subtractions. If your income is $100,000, and you have $20,000 in deductions, then you will pay tax on $80,000 of income.

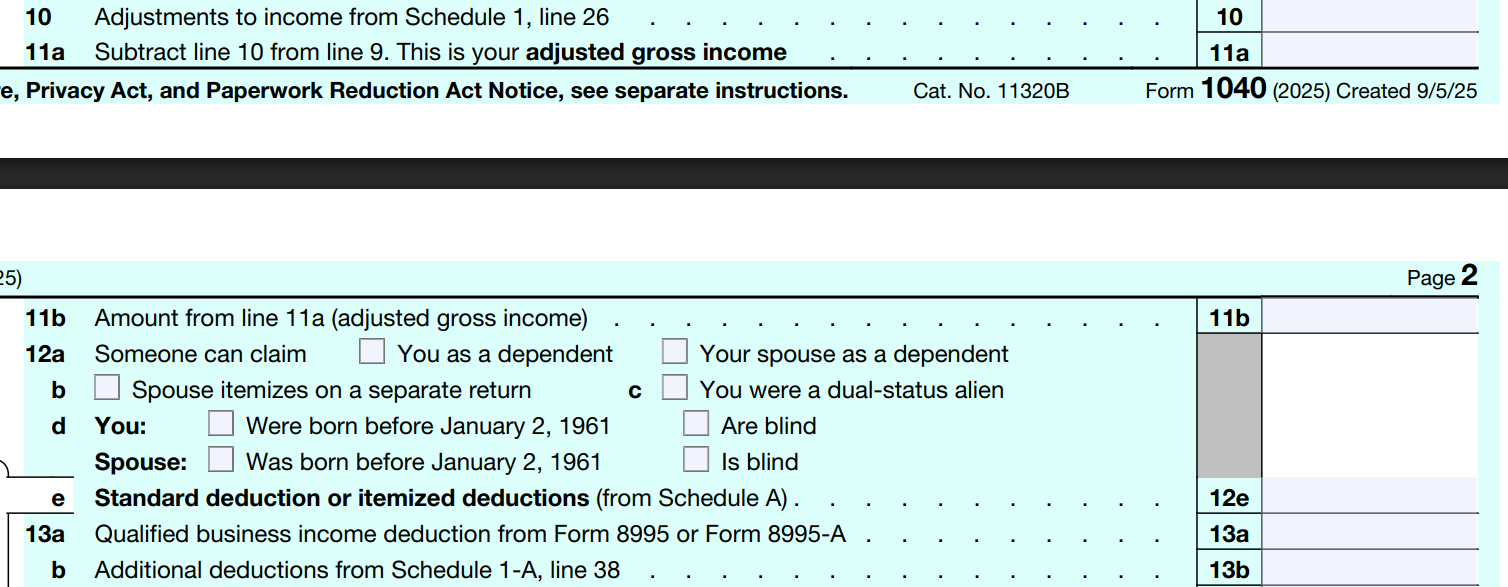

The Deduction Portion of Form 1040

What Deductions Most Likely Need Reviewed?

There are two types of deductions: non-itemized deductions (“above-the-line”) and itemized deductions (“below-the-line”). You will want to review both types of deductions.

Non-itemized deductions can be reviewed using Part II of Schedule 1 and line 10 of Form 1040.

Common deductions that you are likely to utilize as a parent include: student loan interest, contributions to a pre-tax IRA, and contributions to an H.S.A. If you are self-employed, you will want to review your contributions to self-employed retirement plans and any health insurance premiums you pay.

Itemized deductions can be reviewed using Schedule A and line 12e of Form 1040.

As a parent, you are likely to utilize the following deductions: state and local taxes (including income taxes paid and real estate taxes), mortgage interest paid, and gifts to charity.

NEW FOR 2025 TAXES: The most recent tax bill allowed for certain professionals to deduct overtime and tip income. Those deductions can be reviewed using Schedule 1-A and line 13b of Form 1040.

Why Reviewing Your Deductions is Worth Your Time?

Deductions are very easy to overlook! For example, the tax forms for IRA contributions and H.S.A. contributions are not available until May, well after many taxpayers have filed their tax returns. As a result, you are responsible for remembering that you made these contributions.

If you’re married and filing separately. Some of you may find that you and your spouse are better off filing separate returns. Be cautious! Ensure deductions are split evenly (e.g., mortgage interest on jointly held property) or properly assigned to an individual (e.g., IRA contributions). Also, if one spouse itemizes on their return, the other spouse MUST itemize too.

your credits

Tax credits are dollar-for-dollar reductions in your tax bill. It is similar to using a gift card at a restaurant!

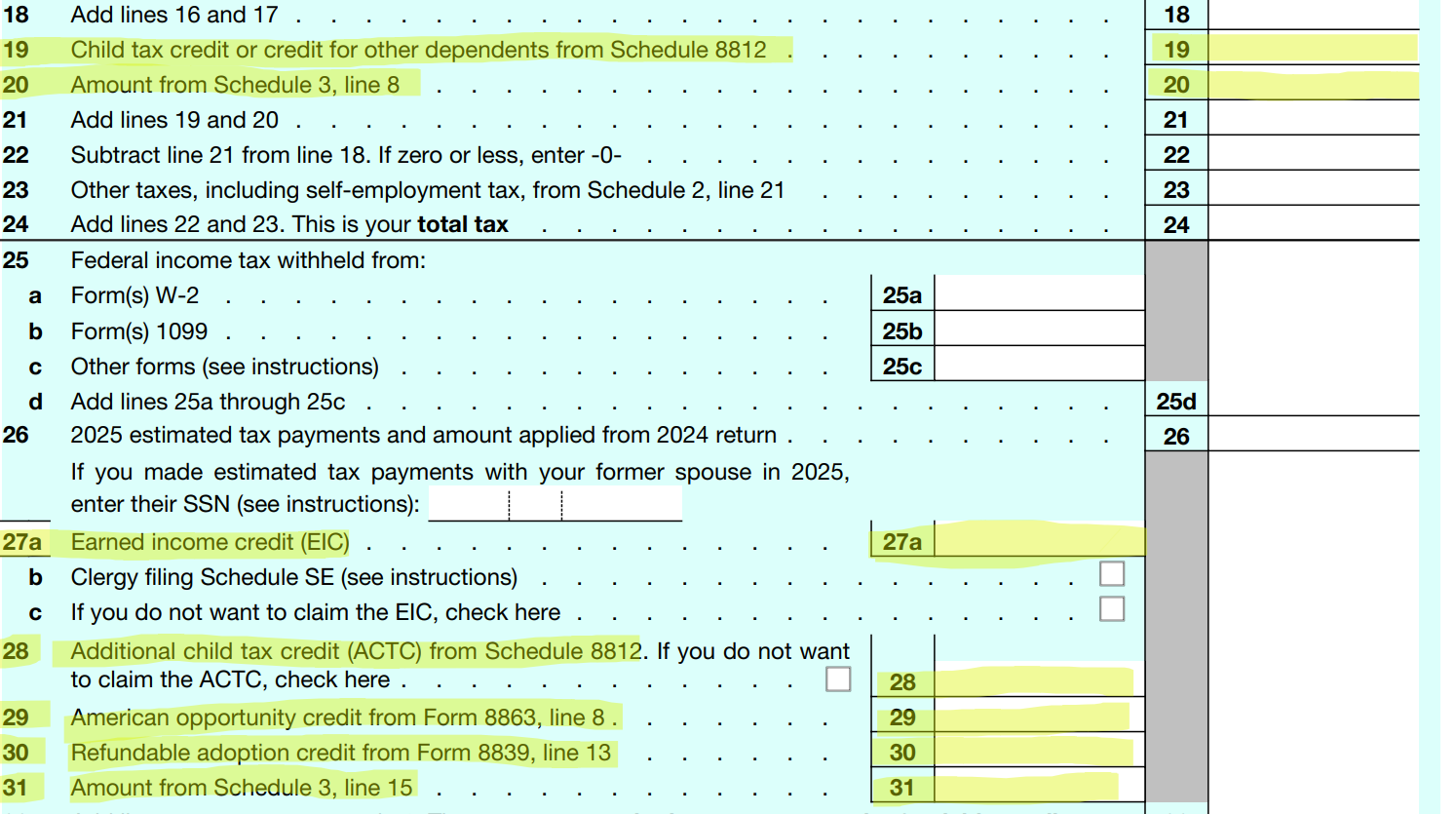

Any credits that you are eligible to utilize will be reported on the second page of Form 1040. Most tax credits are listed on Schedule 3.

Tax Credits Get Reported on Various Lines of Form 1040

Common Credits to Review as a Parent

Unlike deductions, there is no tax form that consolidates all your tax credits for easy review. My recommendation is for you to review each tax form that is generated because you’re eligible for a particular credit.

From my experience, there are 5 popular tax credits amongst parents in their 30s and 40s:

Child Tax Credit

Credit for Other Dependents (usually taken by parents with children age 17 or older)

Child and Dependent Care Credit

Earned Income Credit

American Opportunity Credit (for parents of children pursuing undergraduate degrees)

The Risk of Not Reviewing Your Tax Credits

Credits are the best type of tax break! Let’s say your federal tax bill is $15,000, but you have $3,500 in credits. In this situation, your tax bill drops to $11,500. You should double-check that your tax software has correctly accounted for all available tax credits.

You might still qualify for tax credits, even if it looks like you don’t. Many tax credits have what’s called an income phaseout. Make too much money, and you become ineligible for the full credit. By reviewing specific tax forms and worksheets for credits, you might find that certain tax strategies you can make prior to April 15th will lower your income enough to receive the maximum credit.

contributions to 529 education accounts

The most commonly used account to save for your child’s future college needs is the 529 account.

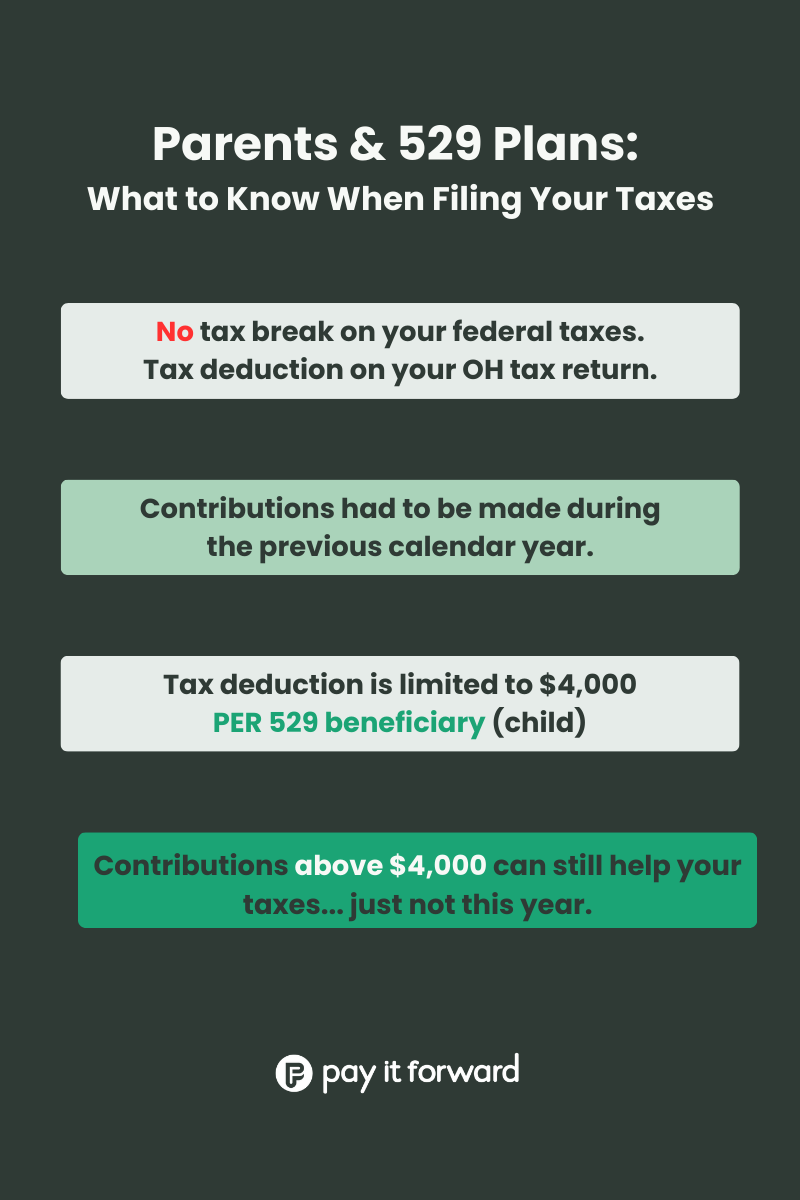

Even though you do not receive a federal tax break for making a contribution, many states, including Ohio, offer a tax deduction.

529 Contributions and Taxes

I’m an Ohio Taxpayer. How Do 529 Contributions Help?

Just like federal tax deductions, OH tax deductions help reduce the amount of income that is subject to OH taxation.

You may deduct $4,000 per beneficiary per year. This is a ‘per return’ limit, meaning married tax filers and single tax filers use the same $4,000 per beneficiary per year limit.

Example: Jeff, 36, and Erin, 34, have two children. Jeff and Erin contribute $3,000 to their son’s 529 plan and another $3,000 to their daughter’s plan.

Jeff and Erin may deduct $6,000 in 529 contributions because the $4,000 per-beneficiary limit was not reached for either child.

Example: Jeff, 36, and Erin, 34, have two children. To maximize long-term growth, Jeff and Erin front-load their contributions, putting $10,000 into their son’s 529 plan and $10,000 into their daughter’s plan.

Jeff and Erin can deduct a total of $8,000 in 529 contributions THIS YEAR - $4,000 for their son and $4,000 for their daughter. The remaining $12,000 in contributions carries forward to future tax years. That is, they are eligible as a deduction, but you have to wait until future years to receive the tax break. Jeff and Erin could take another $8,000 in 529 contributions on next year’s taxes, and use the last $4,000 in contributions on their tax return two years from now.

What Information Should I Double Check?

Recordkeeping is extremely crucial for taking 529 deductions because no tax form is issued.

I recommend downloading the contribution history from your 529 account provider. Also, I recommend that you document the following information:

The name of each beneficiary

The dollar amount contributed during the tax year to each beneficiary’s plan

The amount of unused (carried forward) contributions per beneficiary

your filing status

Your filing status is largely out of your control. For example, an unmarried individual cannot file under any married filing status.

However, reviewing your filing status is especially important as a parent and a married taxpayer.

Tax Status is Selected Towards the Top of Form 1040

What Should I Consider When Picking a Filing Status?

If you’re an unmarried parent and can claim your child(ren) as a dependent(s), then you’ll want to make sure you’re filing under the Head of Household status.

If you’re married, you must decide between married filing separately and married filing jointly.

You should ask yourself the following when selecting between MFS and MFJ:

Who’s claiming our children if we file separately?

Does filing separately make us ineligible for any tax deductions or tax credits?

Am I, or my spouse, making student loan payments based on my/their reported income?

The biggest misconception that you can make is simply filing using the tax status that gives you the largest refund.

parting thoughts

So, if you're a parent in your 30s or 40s, you will want to make sure that you've double-checked your dependents, available tax deductions and tax credits, contributions to 529 education plans, and your filing status. These five parts of your tax return play a huge role in helping you lower your tax bill.

I hope this article will help you catch something on your return — or just give you more confidence before hitting Submit! And if you know a fellow parent who could use this, share it with them. It might save them more than just stress!

If you’d rather offload your tax return this year, then check out my Tax Preparation Services.